Credit Reporting is one of the most mis-understood services in our financial lives. Up until a couple of years ago, the credit repositories were not legally obligated to disclose what or how they came up with credit scores. I worked in retail banking and made the mistake of guessing what my clients needed to do to improve their scores.

Perhaps you or someone you know was advised to close a credit card account thinking it would be good, but your credit score got worse. Why? Hopefully the following definitions will help you have a better understanding of your credit report and how different activity can have a dramatic affect on your score. By clicking on the title to this article, you can visit the www.myfico.com credit education site for more information.

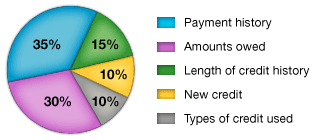

First, it is important to understand that your credit score is a only snapshot of your credit profile at any given point. Any credit activity will change the score as indicated below.

- 35% of Score - Payment History: How well do you pay your credit obligations on time?

- 30% of Score - Amounts Owed: Are your credit cards maxed out?

- 15% of Score - Length of Credit History: How long have your accounts been open?

- 10% of Score - Types of Credit: How diverse are the types of credit you use?

- 10% of Score - New Credit: Doe you apply for credit frequently?

No comments:

Post a Comment